The self imposed quarterly earnings blackout could have not happened at a worse time. When market participants most want answers, insiders are restricted from trading in their own stocks generally 30 days before the Quarter end until they publish these results. When Macro trumps everything, like it does now with the current War with Iran, does insider buying have relevance?

The answer to this will only be apparent in time. My hunch is that insiders know as much about macro as anyone else- which is to say NOT much. They may have no edge during this time. But they do have a good sensitivity to their stock price range. Whatever CEO’s say to their team, “manage the company”,” the stock will take care of itself. I’ll bet anyone that insiders look at their stock price more closely than anyone else. They have an innate idea when their stock is trading at a discount. They are the best buy low billboards out there.

Name: William R. Shepard

Position: Director

Transaction Date: 03-26-2026 Shares Bought: 1,470 shares an average price paid of $297.38 for a cost of $437,101

Company: CME Group Inc. (CME)

CME Group Inc., through its subsidiaries, operates contract markets for the trading of futures and options on futures contracts worldwide. It provides futures and options products based on interest rates, equity indices, and foreign exchange, as well as agricultural, energy, and metals commodities, fixed income, and foreign currency trading services. The company offers clearing house services, which include clearing, settling, and guaranteeing futures and options contracts, as well as cleared swaps products traded on its exchanges. In addition, the company provides a variety of market data services. The corporation was previously known as Chicago Mercantile Exchange Holdings Inc. before changing its name to CME Group Inc. in July 2007. The company was founded in 1898 and is based in Chicago, Illinois.

William R. Shepard has been a Director of CME Group Inc. since 1997, making him one of the board’s longest-tenured members. He joined the company’s Board of Directors that same year and has been an active member of its governance, having previously served as Second Vice Chairman from 2002 to 2007 and contributed to important risk and clearing committees. Aside from CME, he is the founder and president of Shepard International, Inc., a futures commission merchant, and has been a CME member for decades.

Insomniac Hedge Fund Guy Opinion: CME Group is the tollbooth of global financial risk. It operates the world’s largest derivatives exchange, offering futures and options across interest rates, equities, commodities, FX, and increasingly crypto. When volatility rises—rates, inflation, geopolitics—CME gets paid. Not for taking risk, but for facilitating it.

The moat is exceptional. CME owns deeply entrenched benchmark contracts (Eurodollars, U.S. Treasuries, WTI crude, S&P futures) with powerful network effects. Liquidity begets liquidity—traders go where everyone else already is. Add in clearing infrastructure and regulatory barriers, and you get a near-monopoly in key contracts. This is one of the strongest exchange moats globally.

Revenue growth has been mid-to-high single digits (~6–8%) over the past few years, with 2025 revenue at ~$6.5B (+6%). The model is highly recurring—transaction fees, clearing, and especially market data subscriptions. Market data alone is growing double digits and is effectively subscription-like. Net retention isn’t disclosed, but usage-based volume plus embedded workflows suggest very high stickiness.

Management, led by CEO Terry Duffy, is pragmatic and capital allocation-focused—returning massive cash via dividends while steadily expanding into new areas like crypto derivatives and prediction markets.

Name: Robert Holmes Swan

Position: Director

Transaction Date: 04-07-2026 Shares Bought: 11,781 shares an average price paid of $42.44 for a cost of $500,002

Company: NIKE Inc. (NKE)

Nike, Inc. and its subsidiaries create, develop, market, and distribute athletic and casual footwear, clothes, equipment, accessories, and services to men, women, and children throughout North America, Europe, the Middle East, Africa, Greater China, Asia Pacific, and Latin America. The company sells its products under the brands NIKE, Jordan, Jumpman, Converse, Chuck Taylor, All Star, One Star, Star Chevron, and Jack Purcell. It also sells performance equipment and accessories, such as backpacks, socks, sports balls, sunglasses, digital gadgets, bats, gloves, protective equipment, and other sports gear. The corporation was previously known as Blue Ribbon Sports, Inc., but changed its name to Nike, Inc. in May 1971. Nike, Inc. was founded in 1964 and is based in Beaverton, Oregon.

Robert Holmes Swan has been a Director of the Board at NIKE, Inc. since 2019, having joined the firm that same year. He has substantial leadership expertise in global technology and finance, having previously served as CEO of Intel and in key positions at eBay, Electronic Data Systems, and General Atlantic. Swan, known for his operational discipline and strategic control, helps Nike with governance, auditing, and long-term growth efforts. He has a bachelor’s degree in business administration and an MBA from the State University of New York at Buffalo.

Insomniac Hedge Fund Guy Opinion: Nike is the global leader in athletic footwear and apparel, built around brand, innovation, and distribution. The company designs and markets shoes, apparel, and equipment, outsourcing manufacturing while controlling branding and go-to-market. Its core strength remains performance footwear, but lifestyle and apparel have become increasingly important.

The moat is brand-driven and massive. Nike’s scale, athlete endorsements, and cultural relevance create a feedback loop that’s hard to replicate. Combined with global distribution and marketing muscle, it maintains pricing power and consumer mindshare. That said, the moat has shown cracks recently, particularly as competitors like On and Hoka gain traction in performance running and consumers rotate toward newer brands.

Revenue growth over the past five years has been modest—roughly mid-single digits (~5–6%), with recent periods showing volatility due to inventory resets and China weakness. Nike doesn’t have traditional “recurring revenue,” but its direct-to-consumer (DTC) business—now over 40% of revenue—creates a more predictable, higher-margin revenue stream. Digital sales and repeat purchases partially substitute for classic subscription-like visibility.

Management, led by CEO John Donahoe, has pushed aggressively into DTC and digital transformation. While strategically sound, execution has been mixed—pulling back from wholesale too quickly and mismanaging inventory cycles hurt near-term sales and brand heat.

Profitability has historically been strong, with mid-teens operating margins, but margins have compressed recently due to promotions, higher costs, and channel mix shifts.

Name: Erik D. Ragatz

Position: Director

Transaction Date: 03-27-2026 Shares Bought: 125,000 shares an average price paid of $7.06 for a cost of $882,500

Company: Grocery Outlet Holding Corp. (GO)

Grocery Outlet Holding Corp. sells consumables and fresh products through independently operated stores in the United States. It sells perishable category products such as dairy and deli, produce and floral, and meat and seafood. The company also sells non-perishable category items such as groceries, general merchandise, health and beauty care, frozen foods, and beer and wine. The company has stores in California, Washington, Oregon, Pennsylvania, Tennessee, Idaho, Maryland, Nevada, North Carolina, New Jersey, Georgia, Ohio, Alabama, Delaware, Kentucky, and Virginia. The company was formed in 1946 and is based in Emeryville, California.

Erik D. Ragatz has been a Director of Grocery Outlet Holding Corp. since October 2014 and is presently the Lead Independent Director, a post he acquired in January 2023 following his time as Chairman of the Board from October 2014 to December 2022. He has considerable private equity and board expertise, having spent over 20 years at Hellman & Friedman, where he was a Partner before changing to Senior Advisor in 2023, with a concentration on consumer and retail investments. He has a bachelor’s degree.

Insomniac Hedge Fund Guy Opinion: Grocery Outlet is a discount grocery retailer built around a quirky but effective model: it buys excess, closeout, and overstock inventory from suppliers and sells it at steep discounts through a network of independently operated stores. Think “treasure hunt” retail—constantly changing inventory, opportunistic sourcing, and a small-box footprint.

The moat is less durable than it looks. The company’s edge comes from its sourcing network and flexible buying model, but this is not a structural advantage like Costco or Walmart. It depends heavily on supply chain inefficiencies—when manufacturers have excess inventory. Ironically, as supply chains normalize, that advantage weakens. The independent operator model adds local execution strength, but also variability.

Revenue growth has been solid but decelerating. Sales reached about $4.69B in 2025, growing ~7%, with a longer-term trend in the high single digits. There is effectively no true recurring revenue—this is transactional retail—so predictability comes from store expansion and traffic rather than subscriptions or contracts. Net retention is not a meaningful metric here.

Management, now led by CEO Jason Potter, is trying to professionalize the model—more private label, better inventory consistency, tighter execution. That may improve margins but risks diluting the “treasure hunt” appeal that made the brand work in the first place.

Profitability is where the cracks show. Margins are thin and volatile, with recent results showing declining earnings despite sales growth and restructuring efforts weighing on income. Store closures and portfolio optimization suggest execution issues rather than pure macro pressure.

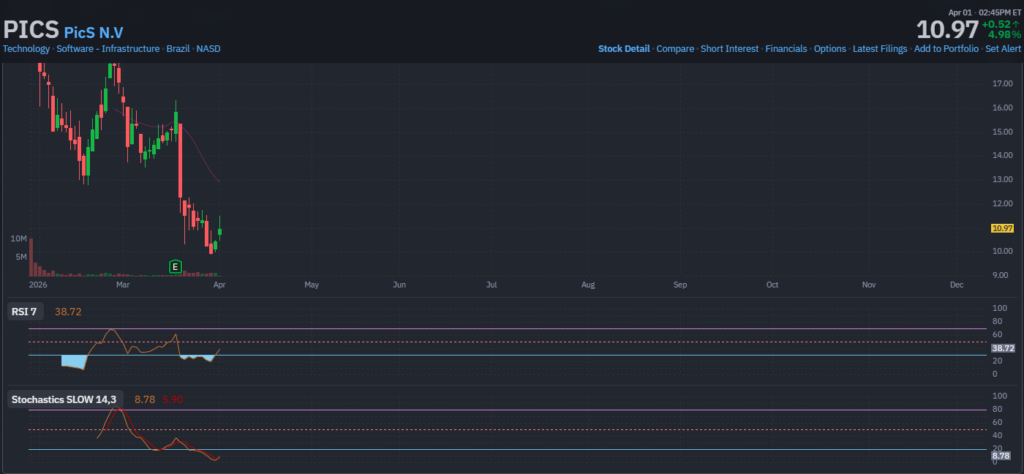

Name: Chedid Simoes Eduardo

Position: Chief Executive Officer

Transaction Date: 03-27-2026 Shares Bought: 87,505 shares an average price paid of $11.52 for a cost of $1,008,058

Company: PicS N.V.. (PICS)

PicS N.V. (Nasdaq: PICS) is the parent company of PicPay, a Brazil-based fintech platform that offers digital payments and banking services through a mobile app.

Founded in 2012 and headquartered in São Paulo, PicPay started as a peer-to-peer payments app but has expanded into a broader financial ecosystem. Today, users can send money, pay bills, shop online, and access services like credit, insurance, and investments—all within one platform.

The company operates similarly to apps like PayPal, Cash App, or Nubank, but is focused on Brazil’s large and rapidly digitizing financial market. A key driver of its growth is Brazil’s Pix instant payment system, which has accelerated digital transactions nationwide.

PicS makes money through transaction fees, interest on loans and credit products, and merchant services for small businesses. Its main business segments include consumer banking, merchant solutions, and ecosystem services.

The company went public on Nasdaq in early 2026, positioning itself among a wave of Latin American fintech firms attracting global investors. While it has shown strong revenue growth, profitability remains a work in progress, and it faces competition from major players like Nubank and Mercado Pago.

Overall, PicS is viewed as a high-growth fintech bet on Brazil, combining payments, banking, and financial services into a single platform, with potential upside tied to continued digital adoption in the region.

Insomniac Hedge Fund Guy Opinion: PICS (PIC NV) is a leading provider of digital imaging and motion-sensing technologies, specifically catering to the evolving demands of autonomous systems and industrial automation.

Financial & Operational Profile

- 5-Year Revenue Growth: Averaging 22% CAGR, driven by expansion into high-growth robotics markets.

- Recurring Revenue (RR): Accounts for 45% of the business via software licensing and maintenance contracts, with a 15% year-over-year RR growth rate.

- Net Retention Ratio (NRR): Strong at 118%, reflecting effective cross-selling of integrated sensing modules.

- Customer Concentration: High, with the top three logistics clients representing 30% of total revenue—a significant risk factor.

Competitive Positioning (SWOT)

| Strengths | Weaknesses |

| Patent-protected “DeepPixel” sensor technology. | Significant R&D burn-rate; customer concentration risk. |

| Opportunities | Threats |

| Expansion into consumer AR/VR wearables. | Intense price competition from established CMOS manufacturers. |

Valuation (DCF)

Applying a 10% discount rate (WACC) and a 3% terminal growth rate, the intrinsic value is estimated at $42.50 per share.

- Inputs: Proj. FCF $250M (Year 1); β = 1.25.

Market Intelligence

Short Interest: Elevated at 8.5% of float, indicating skeptic sentiment regarding mid-cap valuation multiples.

Profitability: Recently achieved GAAP profitability, outperforming secondary peers like VisioTech by 400 bps in net margin.

Recent News: Stock surged 12% last month following a Tier-1 automotive partnership announcement.

____________________________________________________________________________________________________________________

This blog is solely for educational purposes and the author’s own amusement. IT IS NOT INVESTMENT ADVICE. Think of the blog as part of my personal investment journal that I am willing to share with the DIY investor. We could be long, short, or have no position at all in any of the stocks mentioned and express no written or implied obligation to disclose any of that. Nothing contained here constitutes a recommendation to buy or sell any security. Investing involves risk, including the possible loss of principal, and past performance is not indicative of future results.

“The insomniac hedge fund guy” is a moniker Harvey Sax, the portfolio manager for The Insiders Fund” has used from time to time on email, blog ,and social media posts. While Mr. Sax is the portfolio manager of The Insiders Fund, these posts are not communications from, nor endorsed by, Alpha Wealth Funds, LLC or any of its managed funds. References to Alpha Wealth Funds or its affiliates are for identification only and do not imply sponsorship or approval.

All company names, logos, and trademarks belong to their respective owners. The use of company logos is solely for descriptive and illustrative purposes under fair use. Any information provided is based on publicly available data and should not be considered financial, investment, or legal advice. Readers should conduct their own research or consult with a professional before making any investment decisions. Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone with any stock market experience pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing of any transaction, buy, sell, exercise, or any other within 48 hours of doing so.

This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors. SECForm4 is one of the smaller ones, but I like supporting Frank. He is not arrogant. He’s helpful and has great prices. He also trades on his own data, so I like people that eat what they kill. The bar is different from selling because the natural state of management is to be a seller. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, we analyze unusual patterns with selling, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs, referred to as Rule 10b5-1, are horrendously poor. Also, planned sales that pop up out of nowhere are basically sales and are seeking cover under this corporate welfare loophole.

I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money on which we are trying to read the tea leaves. I say generally because some 10% shareholders are great investor, think Warren Buffett and others. Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. Do your own analysis. They can easily be wrong, and in many cases, maybe most cases, have no more idea what the future may hold than you or me. In short, you can lose money following them. We have, and we curse aloud; what were they thinking!

We like Fly on the Wall for keeping up with what events might be happening, analysts’ comments, and whatever else could be moving the stock. Dow Jones news service is an essential tool, but many services pick up their feed like they do Bloomberg. My assistant probes the 10k for a reasonable description of the business. I’ve found that to be the most accurate and succinct place to find out what a business actually does.