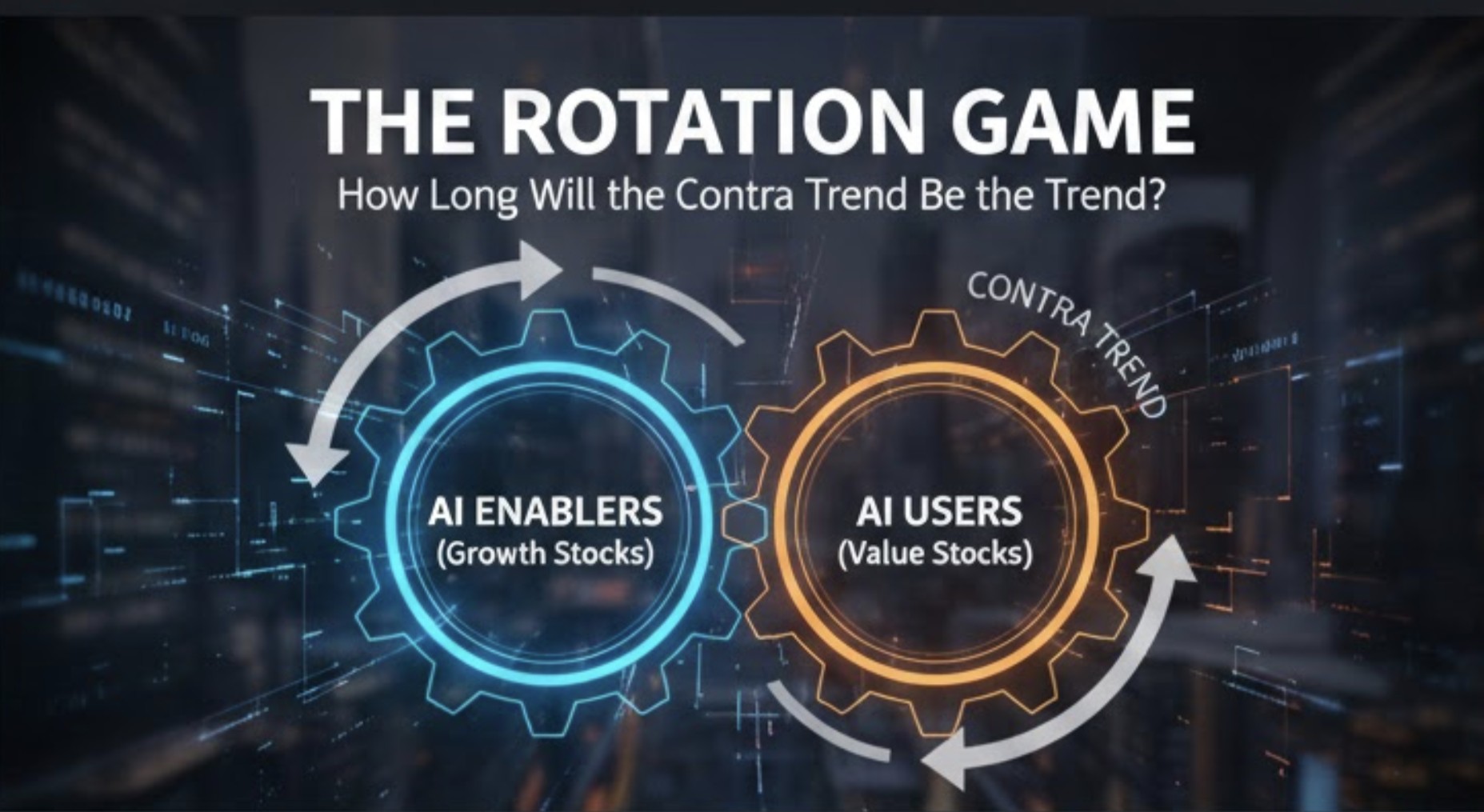

There’s a developing theme from last week’s trading action. It’s not that AI isn’t the real deal, but rather the real beneficiaries are the hundreds if not thousands of companies that can deploy it to solve fundamental business challenges like just-in-time inventory, freight management, help desk support, assembly line automation, legal, and yes, hedge funds banking cash. It’s the almost endless ways AI can improve productivity.

The broadening out of the market was apparent as the companies most credited with the AI productivity boom were the losers, not the winners. A vivid example on Friday was Apple up, Google down.

The popular consensus is that hyperscalers are spending money to get to AGI. There is no second place. If they don’t get there first, their franchises are toast. It’s existential. That’s why Zuckerberg is paying billion-dollar signing bonuses. They have irrational capex expenditures, and the real beneficiaries may be the rest of the market. The answer to that riddle will take months, maybe years to unravel. The important question is: how long will the contra trend be the trend?

Name: Henry A. Fernandez

Position: Chairman and CEO

Transaction Date: 12-05-2025 Shares Bought: 12,500 shares an Average Price Paid of $536.14 for Cost: $6,701,732

Company: MSCI Inc.(MSCI)

MSCI Inc. is a prominent provider of vital decision support tools and solutions for the worldwide investing community, providing mission-critical services to help investors negotiate the complexity of an ever-changing financial landscape. MSCI provides customers with significant knowledge of the global investment process, as well as expertise in research, data, and technology, enabling them to assess key risk and return drivers and build more successful portfolios. The organization has a thorough understanding of client needs, challenges, and objectives, enabling proactive responses to industry developments. MSCI is committed to an integrated approach, service quality, and new research, and it ensures that its solutions are accessible through adaptable, cutting-edge technology.

Henry A. Fernandez has been a director and Chairman of the Board since November 2007, and the CEO since 1998. He served as President from 1998 to 2017. Before leading MSCI’s transformation into a fully independent, publicly traded company in 2007, he worked at Morgan Stanley as a Managing Director, where he was responsible for emerging markets product strategy, equity derivative sales and trading, mergers and acquisitions, global corporate finance, and mortgage finance for US financial institutions. He worked with Morgan Stanley from 1983 to 1991, and again from 1994 to 2007. He earned a Bachelor of Arts in Economics from Georgetown University, an MBA from Stanford University’s Graduate School of Business, and a doctorate in Economics from Princeton University.

Insomniac Hedge Fund Guy Opinion: MSCI is a classic data-royalty compounder: entrenched infrastructure, sticky recurring revenue, and pricing power rare in financial services. Its competitive moat comes not from scale alone but from embeddedness in global asset allocation workflows — switching costs are real, and retention metrics reflect that. Insider buying by Fernandez at levels north of $530 calls BS on near-term market angst and underscores management’s belief in the long trajectory. Short interest hovers low, consistent with the quality story, not a value trap. That said, market pricing isn’t screaming cheap — premium multiples persist because investors are betting on secular passive inflows and monetization of new data products. The biggest risks are slower net new sales and index competition, but the durable, predictable revenue base and robust margins give this compounder optionality few rivals match. In short: high-quality moat, predictable cash flows, priced for perfection — attractive for long-term compounders who can stomach near-term growth cycles and valuation compression. Not financial advice — just one seasoned market brain’s terse take.

Name: Timothy C. Stonesifer

Position: Director

Transaction Date: 05-12-2025 Shares Bought: 962 shares an Average Price Paid of $311.73 for Cost: $299,884

Company: Insulet Corp (PODD)

Insulet Corporation develops and manufactures insulin delivery systems for individuals with insulin-dependent diabetes in the United States and worldwide, including the Omnipod 5 automated insulin delivery system and the Omnipod DASH platform, both of which utilize Bluetooth technology for insulin management and are integrated with continuous glucose monitoring. The company also produces delivery pods for Amgen’s Neulasta Onpro kit, designed to reduce the risk of infection after chemotherapy. Insulet sells its products to pharmacies and independent distributors. The company was founded in 2000 and has its headquarters in Acton, Massachusetts.

Timothy C. Stonesifer serves as a director of Insulet Corporation, having been appointed to the board on January 18, 2024. He has been a seasoned finance executive since April 2019. He has been Chief Financial Officer at Alcon Inc. Before that, he held CFO and senior-finance roles at several major companies, including Hewlett Packard Enterprise, General Motors, and divisions of General Electric, among others. He brings deep financial expertise and global operational insight to Insulet, qualifying as an “audit committee financial expert. Education-wise, he earned a Bachelor of Arts in Economics from the University of Michigan.

Insomniac Hedge Fund Guy Opinion: The gorilla in the room is GLP 1 drugs and the new drugs coming in the market that have the market cowed that diabetes might have a cure or at a minimum a much reduced market.While the initial announcement of highly effective GLP-1s caused volatility in Insulet’s stock (PODD), the company appears to be well-positioned for resilience due to:

-

Insulin Necessity: The fundamental and enduring need for insulin delivery devices in the T1D market and in advanced T2D.

-

Product Superiority: The competitive advantage of the tubeless, user-friendly Omnipod 5 AID system, which fosters high patient retention.

-

Growth Strategy: A clear path for growth by expanding T2D penetration and diversifying into non-insulin drug delive

- Under-Penetrated Markets: Insulet has significant room for growth, even in its established markets. Management has noted low penetration in the T1D market (e.g., ~40% in the U.S.) and even lower penetration in the insulin-requiring T2D market (less than 5% in the U.S.).

Not financial advice — just a cold look at the data.

Name: David Smith Byron Jr.

Position: Director

Transaction Date: 12-10-2025 Shares Bought: 6,709 shares an Average Price Paid of $250.13 for Cost: $1,678,122

Company: Illinois Tool Works Inc. (ITW)

Illinois Tool Works Inc. is a global industrial producer that produces specialized products and equipment for the automotive, food, test and measurement, electronics, welding, polymers and fluids, construction, and specialty product markets. Through direct sales and distributors across the world, the company serves a diverse variety of end markets such as automotive, construction, commercial food service, industrial production, and MRO. Illinois Tool Works Inc., founded in 1912, is headquartered in Glenview, Illinois.

David S. Byron Smith Jr. is a director of Illinois Tool Works Inc., having joined the board on December 4, 2009. He has extensive legal and governance experience, having previously served as Executive Vice President for Policy & Legal Affairs and General Counsel at the Mutual Fund Directors Forum, where he gained expertise in regulatory monitoring and corporate governance. Previously, he held high legal positions at the Securities and Exchange Commission, including Associate Director in the Division of Investment Management. Smith received his bachelor’s degree from Carleton College, followed by a master’s degree in English from the University of Chicago and a Juris Doctor, magna cum laude, from Harvard Law School.

Insomniac Hedge Fund Guy Opinion: ITW is a Grinderman industrial — not a rocket stock, but a cash-generating machine with enviable margins and shareholder returns. Its moat isn’t sexy recurring revenue but disciplined execution and portfolio diversification. Top-line growth is snail-paced, which chills growth investors and invites short interest — but the company’s strong FCF and disciplined buybacks cushion valuation risk.

Name: Stephen G. Pagliuca

Position: Director

Transaction Date: 12-10-2025 Shares Bought: 43,300 shares an Average Price Paid of $229.57 for Cost: $9,940,341

Company: Gartner Inc. (IT)

Gartner, Inc. is a global research and consultancy firm that delivers insights and direction to leaders in a variety of industries. It conducts research, conferences, and consulting. It provides subscription-based research, data, benchmarks, expert access, executive events, and advisory services in areas such as digital transformation, IT strategy, cost optimization, and sourcing. Gartner was founded in 1979 and is based in Stamford, Connecticut.

Stephen G. Pagliuca has been a director of Gartner Inc. since 1990, with a brief absence in 2009 when he stepped out to run for the United States Senate, before rejoining the board in 2010. He is a senior advisor, former Managing Director and Co-Chairman of Bain Capital, and has extensive experience in corporate strategy, private equity, and global leadership. He also owns and leads significant sports clubs. Pagliuca started his career as a senior accountant and international tax specialist before joining Bain & Company in 1982. He then co-founded the Information Partners private equity fund for Bain Capital in 1989. He received a bachelor’s degree from Duke University and an MBA from Harvard Business School.

Insomniac Hedge Fund Guy Opinion: Gartner’s down over 50% YTD. It’s value is real: high-margin recurring revenue, entrenched enterprise clientele, and an enviable cash flow profile. But the stock’s recent valuation has been hammered for good reason — growth is slowing, and the traditional research model is under pressure from digital-first competitors and tighter IT budgets. Knowledge workers are threatened no doubt by AI but the heavy share buybacks hint that management sees intrinsic value. Focus on cash flows and retention quality, not fantasy growth multiples. This is not advice, but a seasoned market vet’s take: solid business, modest runway, don’t overpay for nostalgia but a $10 million insider buy is still real money.

Name: Kenneth S. Courtis

Position: Director

Transaction Date: 12-08-2025 Shares Bought: 36,000 shares an Average Price Paid of $175.26 for Cost: $6,309,390

Company: Alpha Metallurgical Resources Inc. (AMR)

Alpha Metallurgical Resources, Inc. is a mining company engaged in the production, processing, and sale of metallurgical and thermal coal in Virginia and West Virginia. The company specializes in high quality metallurgical coal used in steelmaking. It operates twenty active mines along with eight coal preparation and loading facilities. Formerly known as Contura Energy, Inc., the company adopted the name Alpha Metallurgical Resources, Inc. in February 2021. Founded in 2016, it is headquartered in Bristol, Tennessee.

Kenneth S. Courtis has been a director of Alpha Metallurgical Resources Inc. since February 2021, joining the board as an independent member shortly after the company shifted its focus to metallurgical coal production. He brings more than thirty years of experience in corporate finance, commodity markets, and global investments, shaped by senior roles such as vice chairman and managing director at Goldman Sachs and chief economist and investment strategist at Deutsche Bank Asia. His background adds strong governance and strategic insight to AMR’s board. He completed his undergraduate studies at Glendon College in Toronto, earned a master’s degree in international politics from the University of Sussex, obtained an MBA from the European Institute of Business Administration, and received a doctorate with high distinction from Sciences Po in Paris.

Insomniac Hedge Fund Guy Opinion: Alpha Metallurgical isn’t a ‘moated growth story’; it’s a cyclical commodity play with a solid balance sheet and cost discipline. When metallurgical coal pricing and steel demand recover, AMR has the leverage to outperform — but today’s earnings and revenue trends paint stress, not strength. Insider buying suggests management believes the worst may be priced in or that share repurchases deliver more bang for the buck than reinvestment in capex. The elevated short interest reflects skepticism on near-term demand and margin compression. At current levels, valuation looks fair to cheap on a depressed earnings baseline, yet there’s scant margin of safety without a demand rebound. This isn’t a buy-and-hold compounder — it’s a cyclical turnaround watch, dependent on global steel markets and coal pricing dynamics. Not investment advice — just boots-on-the-ground bearish-meets-value reality.

Name: Stephen N. Landsman

Position: EVP, General Counsel

Transaction Date: 12-12-2025 Shares Bought: 3,100 shares an Average Price Paid of $63.48 for Cost: $196,788

Company: International Flavors & Fragrances Inc. (IFF)

International Flavors and Fragrances Inc. is a global manufacturer of ingredients and solutions for the food, beverage, health and biosciences, perfume, and pharmaceutical industries. The company is divided into four segments: Nourish, Health and Biosciences, Scent, and Pharma Solutions. It provides natural-based food additives, flavors, perfumes, enzymes, cultures, and pharmaceutical excipients for use in consumer, industrial, and healthcare industries around the world. International Flavors & Fragrances Inc. was founded in 1909 and is located in New York, NY.

Stephen N. Landsman is the Executive Vice President and General Counsel of International Flavors & Fragrances Inc., a position he assumed in May 2025. He is in charge of legal, compliance, and corporate governance, having previously held top positions at Syngenta, Univar, and Nalco. Previously at IFF, he oversaw business growth projects. Landsman received his bachelor’s and law degrees from the University of Illinois and is a Certified Public Accountant.

Insomniac Hedge Fund Guy Opinion: IFF is a real industry workhorse with entrenched customer relationships and diversified product lines across necessity-adjacent categories. But unlike a tech or healthcare disruptor, its growth engine sputters in a low-growth, cyclical landscape, and its historical over-paying for DuPont assets still casts a shadow. The stock’s current valuation seems to assume steady but uninspiring execution, with recent insider buying hinting management sees stabilization ahead. That said, absent a clear catalyst to turn the top line into durable organic growth, the margin of safety is slim — and long holders are really betting on operational overhaul plus activist-driven strategic clarity. It’s a value play with structural risk, not a growth compounder. In this business, execution precision matters more than scale.

Name: Chuck Kyrish

Position: SVP & CFO

Transaction Date: 12-09-2025 Shares Bought: 5,000 shares an Average Price Paid of $41.03 for Cost: $205,150

Company: Celanese Corp. (CE)

Celanese Corporation is a multinational chemical and specialized materials company that develops and sells tailored polymers and acetyl products used across automotive, medical, industrial, consumer electronics, construction, filtration, energy storage, packaging, and many other industries. Its Engineered Materials segment produces a wide range of advanced polymers and thermoplastics, while its Acetyl Chain business manufactures essential acetyl products including acetic acid, vinyl acetate monomers, emulsions, and resins that support coatings, adhesives, textiles, packaging, and consumer applications. Celanese markets its products under recognized brands such as Celanyl, ECOMID, Zytel, Celcon, Hostaform, Celanex, GUR, Vectra, Forprene, Santoprene, Vamac, and VitalDose. The company serves customers directly as well as through distributors, including original equipment manufacturers and suppliers. Celanese was founded in 1912 and is headquartered in Irving, Texas.

Chuck B. Kyrish is the Senior Vice President and Chief Financial Officer of Celanese Corporation, a role he assumed on November 8, 2023. He joined Celanese in 2006 and has since held a series of key finance leadership positions, including Financial Risk Manager, Assistant Treasurer, Vice President Treasurer, Vice President of Investor Relations, and Chief Financial Officer of the Acetyl Chain. He brings extensive experience in corporate finance, accounting, treasury, internal audit, and tax functions to his leadership of Celanese’s financial organization. Chuck earned a Bachelor of Science from the University of Texas at Austin and an MBA from Texas Christian University, reinforcing the depth of his financial and executive expertise.

Insomniac Hedge Fund Guy Opinion: Celanese is a gritty industrial with real assets and meaningful cash flows — but it’s drowning in cyclical headwinds and balance-sheet drag. Weak end-markets and pricing pressure have crushed profits and forced drastic measures (dividend cuts, restructuring, asset sales). The recent insider buys are interesting but not a screaming bullish signal — seasoned operators play value at depressed prices with risk controls, not blind optimism. The stock’s valuation bifurcation with its long-term DCF suggests potential optionality if demand recovers and cost actions stick, but the leverage load and weak earnings paint a harsher reality than most chemical peers. Celanese is not yet a core compounder — it’s a turnaround story priced as one, and that’s why shorts haven’t capitulated. Caution and deep due diligence are non-negotiables here. Not financial advice — just a brutally honest market perspective.

Name: Gregory T. Lucier

Position: Director

Transaction Date: 12-05-2025 Shares Bought: 100,000 shares an Average Price Paid of $3.69 for Cost: $368,544

Company: Maravai Lifesciences Holdings Inc. (MRVI)

Maravai LifeSciences Holdings, Inc. is a global life sciences company that supplies essential products used in the development of vaccines, therapeutics, cell and gene therapies, and diagnostics. The company supports human disease research and provides solutions across the entire biopharmaceutical development cycle, from discovery to commercialization. Its customers include major biopharmaceutical companies, emerging biotechnology firms, academic research institutions, and in vitro diagnostics developers. Maravai’s portfolio is designed to advance critical stages of biopharmaceutical research and foster innovation across the industry.

Gregory T. Lucier is a director of Maravai LifeSciences Holdings, Inc., having been elected in January 2020. He has over three decades of experience in healthcare and life sciences; prior to joining Maravai, he was Chairman and CEO of Life Technologies (formerly Invitrogen) from 2003 to 2014, and then Chairman and CEO of NuVasive, Inc. from 2015 to 2018, among other senior industry roles. He is currently the Executive Chairman of Corza Health, Inc., and serves on the boards of many other life-sciences companies. He holds a bachelor’s degree in industrial engineering from Pennsylvania State University and an MBA from Harvard Business School.

Insomniac Hedge Fund Guy Opinion: Maravai is a fascinating turnaround watch, not a stable growth compounder. Its pandemic-boosted past inflates long-term growth optics, but recent topline erosion and negative margins expose a brittle economics. Insider buying signals management’s conviction, but tangible improvement has yet to materialize in GAAP profits or predictable recurring streams — a far cry from the predictability that underpins real moats. The stock’s recent run isn’t validation of fundamentals; it’s short covering and sentiment chasing. At current multiples, DCF suggests limited upside without a clear return-to-growth thesis. For this to deserve a premium multiple, Maravai needs secular demand drivers beyond episodic vaccine bursts, material margin improvement, and clear traction in recurring service contracts. As is, it’s a high-beta play with binary outcomes — not a foundation stock for conservative portfolios.

This blog is solely for educational purposes and the author’s own amusement. IT IS NOT INVESTMENT ADVICE. Think of the blog as part of my personal investment journal that I am willing to share with the DIY investor. There are also many parts that I am not willing to share if I think it could influence trading action or be detrimental to the Fund’s partners. We could be long, short, or have no position at all in any of the stocks mentioned and express no written or implied obligation to disclose any of that. Nothing contained here constitutes a recommendation to buy or sell any security. Investing involves risk, including the possible loss of principal, and past performance is not indicative of future results.

“The insomniac hedge fund guy” is a moniker Harvey Sax, the portfolio manager for The Insiders Fund” has used from time to time on email, blog ,and social media posts. While Mr. Sax is the portfolio manager of The Insiders Fund, these posts are not communications from, nor endorsed by, Alpha Wealth Funds, LLC or any of its managed funds. References to Alpha Wealth Funds or its affiliates are for identification only and do not imply sponsorship or approval.

The Insiders Fund and its blogs and posts are not affiliated with, endorsed by, or sponsored by any of the companies mentioned herein. All company names, logos, and trademarks belong to their respective owners. The use of company logos is solely for descriptive and illustrative purposes under fair use. Any information provided is based on publicly available data and should not be considered financial, investment, or legal advice. Readers should conduct their own research or consult with a professional before making any investment decisions. Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone with any stock market experience pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing of any transaction, buy, sell, exercise, or any other within 48 hours of doing so.

This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors. SECForm4 is one of the smaller ones, but I like supporting Frank. He is not arrogant. He’s helpful and has great prices. He also trades on his own data, so I like people that eat what they kill. The bar is different from selling because the natural state of management is to be a seller. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, we analyze unusual patterns with selling, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs, referred to as Rule 10b5-1, are horrendously poor. Also, planned sales that pop up out of nowhere are basically sales and are seeking cover under this corporate welfare loophole.

I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money on which we are trying to read the tea leaves. I say generally because some 10% shareholders are great investor, think Warren Buffett and others. Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. Do your own analysis. They can easily be wrong, and in many cases, maybe most cases, have no more idea what the future may hold than you or me. In short, you can lose money following them. We have, and we curse aloud; what were they thinking!

We like Fly on the Wall for keeping up with what events might be happening, analysts’ comments, and whatever else could be moving the stock. Dow Jones news service is an essential tool, but many services pick up their feed like they do Bloomberg. She probes the 10k for a reasonable description of the business. I’ve found that to be the most accurate and succinct place to find out what a business actually does. When I have time, over the weekend, I’ll add some preliminary analysis to the Opinion at the end. It is largely done now by my AI. Sometimes I won’t update this for a couple of weeks or more. A good way to use this blog is as I do, it’s a reference point and filing cabinet for various stocks with notable insider buying. It’s one of many tools I use.